A cycle-based approach to district budgeting differentiates between operation and investment expenditures and tracks those expenditures for continuous improvement.

Every winter, school and district leaders face the daunting task of developing a budget for the next school year. Often, they will perform a series of choreographed tasks that Marguerite Roza (2022), director of Georgetown University’s Edunomics Lab calls the “budget dance.” Usually running on something close to autopilot, these budget dance moves involve standardized procedures that start with projecting enrollment and revenue, followed by allocating funds to schools and central office departments. At the same time, school and district leaders may assess what adjustments they must make to district spending, including funding any new initiatives or programs, to support the district’s current priorities. Once the school board approves the budget, most expenditures simply become fixtures and roll over year after year.

This process seldom involves leaders systematically scrutinizing existing expenditures for alignment with district goals, efficiency, and return on investment, which could inform decisions about program expansion, downsizing, or discontinuation. Without such scrutiny, budgets become layered over time with programs initiated by various administrations that have different, and sometimes conflicting, goals and employ varying strategies to achieve them, leading to inconsistency and confusion (DuFour, 2003). Continually stacking on new programs also overwhelms schools, drains people’s attention and energy, and causes innovation fatigue and indifference (Reeves, 2020). Yet cutting or downsizing programs to improve coherence and cohesion is rarely considered an improvement strategy.

That’s not to say that cuts don’t happen. But when districts need to cut spending due to budget shortfalls, they tend to make across-the-board cuts. Usually, the finance office determines what percentage of the budget needs to be cut to get it in balance. Then, all schools and departments are asked to sacrifice by cutting their respective budgets by that percentage, regardless of the varying adverse impacts on department operations or services to students and families. As the economy improves and revenue increases, districts return to expansion by piling on new programs. Unlike across-the-board cuts, districts seldom apply across-the-board increases. Unfortunately, this process can create or exacerbate inequity among departments and across schools.

Although this description may be oversimplifying a complex process, it gives a general sense of how many school districts approach budgeting. When funding is tight, district leaders tend to make indiscriminate cuts that can inadvertently lead to greater inequities and lack of cohesion among improvement strategies. When funds are available, the focus returns to adding new programs without examining existing spending and anchoring new spending decisions on the results of that analysis.

The limitations of this approach to developing and executing district budgets have been broadly discussed. To address the shortcomings, new budgeting models such as zero-based budgeting and priority-based budgeting have been attempted. However, many school systems have not been able to navigate out of repeating the same pattern year after year. That raises the question of why.

Root causes

The above approach to budgeting is driven and shaped by three main causes:

- Reliance on problem-driven needs as the dominant factor of budgetary decisions.

- Disconnect between financial management and performance management.

- Human nature when it comes to problem solving and change.

Reliance on problem-driven needs

When making budget decisions, district leaders should evaluate and weigh a multitude of factors, including alignment with priorities, evidence of impact, cost, community support, feasibility of implementation, and coherence with existing programs (Yan & Hollands, 2018). In practice, however, major problems and needs the district faces tend to dominate budget discussions. This emphasis has an overwhelming influence on decision making in two prominent ways.

First, needs don’t just inform how to prioritize competing new spending ideas but often overshadow other factors in budget decisions. Proposals that address what the community and leadership see as the most urgent needs usually are funded, with little consideration to whether schools already are implementing something to address the problem, whether there’s staff capacity to implement the new programs, and how the new programs might impact existing ones and vice versa.

Second, problem-driven budgeting makes leaders hesitant or unwilling to make spending adjustments that involve reducing or discontinuing expenditures. Any such attempt is likely to bring about accusations of taking resources away from students in need, which also helps explain leaders’ dependence on across-the-board cuts for solving budget crises.

Further contributing to this dynamic is the fact that most districts lack the infrastructure to collect other important information about program alignment, impact, and support (Yan & Hollands, 2018) and integrate it into the financial management process.

Disconnect between financial management and performance management

Financial management in education is largely based on public audit or oversight instead of continuous improvement. While the finance team is involved in decisions about launching new programs, managing money and managing programs become separate businesses once the new spending is approved. The finance team often simply monitors compliance with accounting practices, whereas the program team centers their effort on program implementation.

Part of the problem lies in the fact that the chart of accounts, which the finance team relies on for managing funds, is not designed to allow multiple teams to collaborate around spending based on alignment and evidence of impact. Intended to track financial transactions (Hartman, 1988), the chart of accounts used in most states commonly categorizes expenses for accounting and compliance purposes, not for effectiveness and alignment with priorities. Because of that, most school districts have neither incentives nor means to connect financial management with performance management to better leverage dollars for improving student achievement.

Human nature

For educators, taking actions to help students succeed is both an internal calling and external demand from the community. And the default approach to improvement is usually adding new programs. Low attendance? Let’s launch a new attendance initiative. Behavior problems? How about a new behavior intervention?

This tendency to add may be partly due to the research community’s focus on studying effectiveness of novel interventions and strategies. The potentially positive impact of streamlining or consolidating services often is overlooked, if not entirely ignored, by empirical research. Evidence suggests that this tendency to over-rely on addition and overlook subtraction is built upon human instincts (Adams et al., 2022).

Not only are human beings predisposed to make changes through addition, they’re biased against subtractive changes (Klotz, 2021). Evidence from behavior economics suggests that, when confronted with choices, people tend to take the option that “requires the least effort, or the path of least resistance” (Thaler & Sunstein, 2009). If discontinuing a program means upsetting colleagues, creating enemies, and facing angry parents, why would anyone pursue reduction unless forced?

Breaking the cycle

The current budget process seems to be producing exactly what it is designed to produce. The overshadowing influence of needs in decision making, separation of finance from performance, and the human bias toward addition keep leaders from making effective and timely adjustments. To break the cycle of repeating the same “budget dance” year after year, we need to introduce changes to balance how the multitude of factors (Yan & Hollands, 2018) are used for decision making, connect financial management with performance management, and systemize improvement through both addition and subtraction.

We can move beyond the “budget dance” by integrating two changes:

- Differentiating between operation and investment expenditures.

- Building an improvement infrastructure that allows districts to track and manage investment and operation expenditures differently.

Differentiate between operation and investment expenditures

Ideally, district leaders should scrutinize both new and existing spending through the lens of needs and other important factors (Yan & Hollands, 2018), with the existing expenditures reviewed regularly to ensure they are used optimally for student outcomes. However, this has proven challenging without a new framework and processes. One way to address this challenge starts with differentiating between operation and investment expenditures.

Operation expenditures are expenses districts spend to meet legal requirements and basic community expectations. For example, school buildings’ utilities and maintenance costs must be paid for teaching and learning to take place. Under state and federal laws, schools must meet staffing regulations in both quantity and qualifications to provide education and services to students, including those with special needs. Because of these requirements and mandates, funding for operation expenditures can’t necessarily be tied to goals.

In contrast, investment expenditures are expenses districts choose to achieve specific improvement goals. For example, a district might decide to invest in a campaign to boost school attendance or provide merit pay to teachers with the goal of improving student outcomes. Because investment expenditures are goal-oriented, continued funding should be conditional on achieving the goals.

Conceptually, operation expenditures cover the basic functions of a school system, and investment expenditures represent improvement strategies. Although this is an imperfect distinction, it provides a framework for districts to manage the two classes of expenses separately. Specifically, district leaders should ensure improvement strategies embedded in investment expenditures produce results and are cost-effective. At the same time, they should maximize the efficiency and quality of basic functions covered by operation expenditures.

Build improvement infrastructure

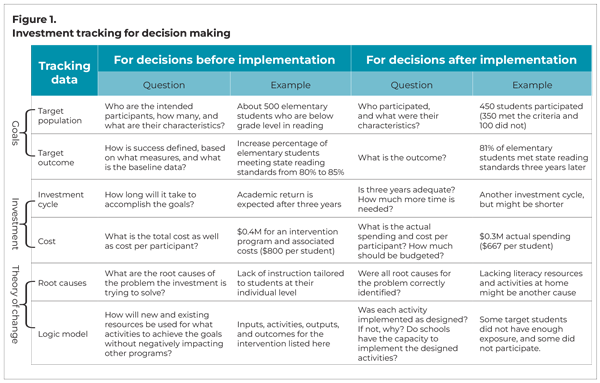

Employing the aforementioned framework, districts can enhance and leverage the budget process to build an infrastructure (Hersh, 2021) for continuous improvement. Under this improvement infrastructure, all new spending begins with a classification decision. For programs and initiatives classified as investment items, each is required to provide seven data points (See Figure 1) so districts can track alignment, implementation, and cost-effectiveness.

In Figure 1, the first column lists the seven data points, with questions decision makers might ask before (column 2) and after (column 4) a program is implemented and examples of possible answers for an elementary school reading intervention.

Each row in the figure represents a different element of the program that leaders should consider:

- Target population and target outcome define what academic return is expected of a new investment and capture its actual return after the program is implemented.

- Investment cycle sets expectations on how much time is needed for the investment to achieve the goals and when it will be reviewed for alignment and return on investment.

- Cost allows district leaders to compare the budgeted and actual spending, which often indicates how well a program is implemented.

- Root causes and logic model are concerned with the theory of change undergirding the investment, how the planned activities relate to the theory of change, and how the planned implementation is executed in the local context and reasons for possible inadequate implementation.

An improvement infrastructure that tracks these data points helps achieve several goals for investment expenditures. First, it informs leaders of the factors they need to evaluate and balance (Yan & Hollands, 2018) when making investment decisions. Second, it lays the foundation for practicing improvement science (Bryk et al., 2015; Lewis, 2015) by requiring that any newly invested program be grounded in a theory of change, coordinated with the existing programs, and regularly assessed and adjusted based on data and evidence. Third, it helps fend off human biases, which favor addition over subtraction, by establishing periodic review of investments as a routine norm.

For spending classified as operation expenditures, a similar cycle-based approach can be employed to conduct periodic benchmark analysis across and within districts. Horizontally, a district can compare itself to similar districts every few years on an array of operations key performance indicators (KPIs), such as those published annually by the Council of the Great City Schools (2022). Under-performing KPIs point to areas where improvements can and should be made by learning from districts with higher efficiencies. Vertically, a district can compare schools, departments, or divisions against efficiency metrics over time. For example, leaders can compare the operation expense per student by school every few years. If the comparison reveals significant increases in one school while the operation expense per student in other schools remains flat, analysis should be conducted to find out why.

If discontinuing a program means upsetting colleagues, creating enemies, and facing angry parents, why would anyone pursue reduction unless forced?

While seeking to increase efficiency of operation expenditures, leaders should also use the process to pursue better outcomes. When thoughtfully designed and successfully executed, districts can both decrease operation costs and increase quality of services that lead to improved student outcomes.

Differentiating between investment and operation expenditures allows districts to manage spending based on different parameters. Creating a cycle-based infrastructure for analysis provides time and space for programs to be fully implemented and show effect, which incentivizes enduring long-term success over potentially unsustainable short-term gain. With adequate time, spending patterns will emerge, which allows leaders to make decisions based on signals rather than noises (Silver, 2015). At the same time, this cycle-based approach makes systematic review of spending transparent, fair, and more manageable. Moreover, it allows leaders to strategically time significant decisions based on cumulative evidence for long-term planning.

Changes offer hope

The annual budget process is a valuable opportunity for district leaders to systematically examine both resource use and district programming and use the findings to inform and drive change to optimize resource use and improve program efficacy for increased student achievement. However, we have not been able to capitalize on the full potential of this opportunity.

When budget decisions are predominantly driven by needs, each established expense is first legitimized and then perpetuated. Since it is difficult to identify and justify one need being more important than the other, adjusting resource use based on needs becomes very challenging. The accounting system districts rely on for managing their financial resources contributes to the disconnect between financial management and performance management.

Differentiating between operation and investment expenditures provides a new framework to manage resources for student success. In this more balanced approach to improvement, the budget process impels leaders to take extra precautions to avoid the “presence of too many disconnected, episodic, piecemeal, and superficially adorned projects,” which is a bigger problem than absence of innovation (Fullan, 2001, p. 109). Following predetermined schedules, leaders can examine both investment and operation expenditures for the purpose of continuous improvement, regardless of the political environment or economic realities. If repeated efforts to improve a program have failed, then subtraction can be considered as a last resort. The mounting evidence accrued over multiple rounds of reviews will make it hard for people to defend and justify such a program’s continuation.

While budgeting is the focal point of our discussion, money is not the central issue here. Ultimately, the goal is to help districts develop disciplined “self-management of improvement” (Elmore, 2003) so that they can provide coherent and coordinated services to students and increase learning outcomes. The two “budget dance” changes we suggest offer new hope and possibilities.

References

Adams, G., Converse, B.A., Hales, A., & Klotz, L. (2022, February 4). When subtraction adds value. Harvard Business Review.

Bryk, A.S., Gomez, L.M., Grunow, A., & LeMahieu, P.G. (2015). Learning to improve: How America’s schools can get better at getting better. Harvard Education Press.

Council of the Great City Schools. (2022). Managing for results in America’s great city schools, 2022: Results from fiscal year 2020-2021.

DuFour, R. (2003). Central-office support for learning communities. The School Administrator, 60 (5), 13-18.

Elmore, R. (2003). Knowing the right thing to do: School improvement and performance-based accountability. National Governors Association Center for Best Practices.

Fullan, M. (2001). Leading in a culture of change. Jossey-Bass.

Hartman, W.T. (1988). School district budgeting. Prentice Hall.

Hersh, D. (2021). The role of RPPs in an education improvement infrastructure. NNERPP Extra, 3 (1), 25-27.

Klotz, L. (2021). Subtract: The untapped science of less. Flatiron Books.

Lewis, C. (2015). What is improvement science? Do we need it in education? Educational Researcher, 44, 54-61.

Reeves, D.B. (2020). The learning leader: How to focus school improvement for better results. ASCD.

Roza, M. (2022, November). Time to change the district budget dance. School Business Affairs.

Silver, N. (2015). The signal and the noise: Why so many predictions fail — but some don’t. Penguin.

Thaler, R.H. & Sunstein, C.R. (2009). Nudge: Improving decisions about health, wealth, and happiness. Penguin.

Yan, B. & Hollands, F. (2018, September). How to prioritize programs for funding decisions? School Business Affairs, 10-13.

This article appears in the March 2024 issue of Kappan, Vol. 105, No. 6, p. 48-52.

ABOUT THE AUTHORS

Bo Yan

BO YAN is the data strategist at Jefferson County Public Schools, Louisville, KY.

Thomas Aberli

THOMAS ABERLI is the director of budget at Jefferson County Public Schools, Louisville, KY.

{kind=link}